Considering home loan prepayment can be a very smart financial decision. If you can afford it, then prepaying can reduce your interest and even shorten your loan tenure. However, it's not simple. You need to understand how prepayment affects your EMIs, tax benefits, and the overall debt to take a smart call. Also, there are conditions to the home loan prepayment feature. Let us understand prepayment well for you to evaluate if it works in your favour.

What is Home Loan Prepayment?

Prepayment of a home loan means you pay a large sum of the remaining debt either in part or in full. If you pay the entire remaining amount, it leads to foreclosure of the loan. However, when you make a part payment, you reduce the principal debt amount, which affects the interest amount or the loan tenure. Depending on the options offered by the lender, you may choose one or both.

Why You Might Consider It?

- Interest savings: Prepayment reduces the total interest cost to a large extent, of course, depending on the amount you pay.

- Shorter tenure: You may choose to close the loan right away or sooner.

- Lesser EMI: Prepayment may reduce your EMI amount by reducing the Principal borrowed amount. You can use tools like the UBI Home Loan EMI calculator to see how much difference it will make.

- Better cash-flow eventually: Lesser EMI or reduction in tenure means lesser debt and more cash in hand. It means improved purchasing power, which you can use to buy or invest in other things.

- Credit profile: Reducing your debt early is good for your credit profile. It improves your debt-to-income ratio and shows that you can pay back loans better. Therefore, it becomes easier for you to take more loans based on your credit score and profile.

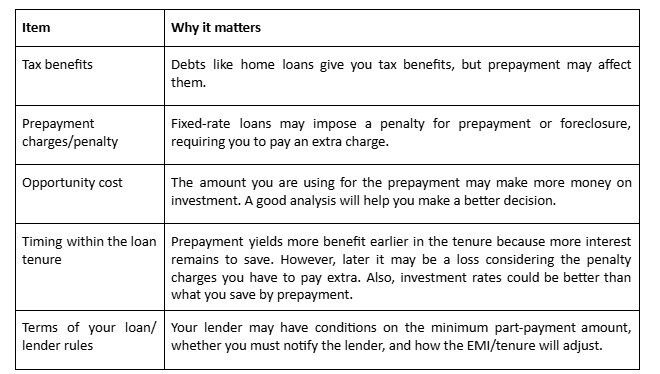

What to Check Before You Prepay?

Before you decide on prepayment, you should examine several components:

Consider comparing the terms across lenders on Bajaj Markets. Being a digital marketplace, it gives you access to multiple home loan options from different lenders in one place, with their prepayment policies transparently. The comparison may help you make better decisions.

Tax Implications: A Key Consideration

You must be aware of how prepayment may impact your tax benefits:

- Section 80C gives you an exemption of up to ₹1.5 lakh per year on home loans.

- Section 24(b) gives you an exemption on the interest paid on home loans of up to ₹2 lakh per year for self-occupied properties. And for rented properties, the entire interest amount is eligible for deduction. (old tax regime)

- If you fully prepay your loan early, you may stop getting these benefits in future years.

- The “new tax regime” doesn’t give any tax benefit on loans. Thus, prepayment may become a more profitable option in the broader sense.

Role of the UBI Home Loan EMI Calculator

The UBI Home Loan EMI calculator helps you understand how prepayment can affect your EMI. You can find out:

- How much interest will you pay on the new debt amount after the prepayment? (Formula: Principal Debt - Prepayment Amount = New Principal)

- You can use the new interest amount to calculate how much total interest you are saving with prepayment. (Formula: Previous Total Interest Amount - New Total Interest Amount + Penalty = Savings)

- You can also use the calculator to check how the new principal loan amount can affect your loan tenure or EMI or both.

- These calculations give you a clear picture on what to expect from the prepayment and whether it's going to be helpful to you.

When Might You Hold Off?

In some cases, it may make sense to delay prepayment if:

- You are expecting higher returns on investments than your loan interest rate with the same amount.

- You are considering using the funds for a near-term major expense (education, health, business).

- Your loan has a minimal interest rate, and you are utilising tax benefits from it.

- You are still in the lock-in period, and the lender does not allow you to prepay.

Conclusion

If you hold a home loan, prepayment is an option you should evaluate seriously. The simple UBI home-loan EMI calculator can help you calculate, compare, and analyse interest savings, tax impact, and opportunity cost. Prepayment can save you money and free you from debt sooner. But only when you check the numbers, understand your tax position, check penalties, and ensure you retain financial flexibility. Take your decisions based on data, and you will make your home-loan journey smarter.

Top comments (0)