Market Overview:

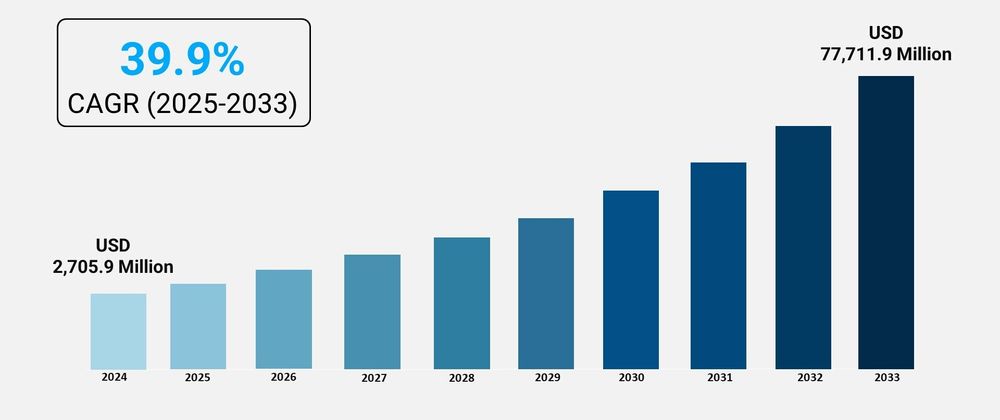

The cloud gaming market is experiencing rapid growth, driven by increasing 5g and high-speed internet penetration, the rise of subscription-based gaming models, and expansion of the casual and mobile gamer base. According to IMARC Group's latest research publication, "Cloud Gaming Market Size, Share, Trends and Forecast by Type, Genre, Technology, Gamers, and Region 2025-2033", offers a comprehensive analysis of the industry, which comprises insights on the global cloud gaming market share. the global market size was valued at USD 2,705.9 Million in 2024. Looking forward, IMARC Group estimates the market to reach USD 77,711.9 Million by 2033, exhibiting a CAGR of 39.9% during 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/cloud-gaming-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Cloud Gaming Market

- Increasing 5G and High-Speed Internet Penetration

The global expansion of high-speed internet, especially the deployment of 5G networks, is a crucial catalyst for cloud gaming growth. Cloud gaming's core requirement is low-latency, high-bandwidth connectivity to stream game sessions from remote servers to user devices. Regions with advanced digital infrastructure, such as North America, already account for a significant market share, with the United States alone holding over 87% of its regional market in a recent period, driven by widespread fiber-optic and 5G network access. The superior capabilities of 5G, offering ultra-fast data transfer and reduced lag, are making console-quality streaming viable on mobile devices, which currently represent nearly half of the total global gaming revenue. This technological rollout enables a seamless gaming experience, even for graphics-intensive AAA titles, fundamentally reducing a primary technical barrier for widespread consumer adoption across all major markets.

- The Rise of Subscription-Based Gaming Models

The shift toward subscription-based service models is accelerating market expansion by democratizing access to extensive game libraries. Services like Xbox Game Pass Ultimate and NVIDIA GeForce NOW offer hundreds of titles for a single monthly fee, eliminating the need for expensive, individual game purchases and costly hardware upgrades. This model creates a compelling value proposition, particularly for casual gamers who do not wish to invest thousands of dollars in a dedicated gaming PC or console; analysts note that the average gamer can spend up to $1,000 on a system, while top-end rigs can cost up to $5,000. The subscription model, which already accounts for approximately 70% of cloud gaming revenue, broadens the consumer base by making a vast array of high-quality content instantly accessible across multiple devices, including smart TVs and smartphones, thereby attracting both casual and more dedicated players.

- Expansion of the Casual and Mobile Gamer Base

The cloud gaming market is significantly expanding by tapping into the massive global casual and mobile gamer populations. With over 3.3 billion video game players worldwide, the ability to play high-fidelity games without owning a console or powerful computer removes a substantial financial barrier to entry. Smartphones, which are owned by billions globally, accounted for over 44% of the cloud gaming device market share in a recent analysis, highlighting their dominance as the primary access point. Casual players currently represent the largest segment of cloud gaming users, holding more than 60% of the market share by gamer type. This growth is also supported by government efforts, such as the Indian government's 'MeghRaj' GI Cloud initiative, which seeks to accelerate the deployment of high-performance public compute infrastructure, indirectly supporting the platform's foundation for millions of mobile-first users.

Key Trends in the Cloud Gaming Market

- Convergence with Major Entertainment Ecosystems

A prominent trend is the deep integration of cloud gaming into the broader digital entertainment and streaming ecosystems championed by major technology and media companies. Key industry players are leveraging their existing cloud infrastructure and millions of established users from their non-gaming services, such as video streaming and e-commerce, to onboard gamers. For instance, a leading technology company is using its immense cloud data center network, which recently saw investments exceeding $35 billion, to power its own and partner streaming platforms, ensuring low-latency delivery. This approach provides a significant competitive advantage by bundling gaming with popular non-gaming subscriptions, enhancing customer loyalty, and streamlining the user experience by offering seamless, single-sign-on access to entertainment across smart devices, laptops, and consoles.

- Proliferation of Cross-Platform Interoperability

Cross-platform interoperability is emerging as a defining feature, allowing users to move seamlessly between devices without interrupting their game session. This trend is driven by consumer demand for flexibility, which is essential as players often alternate between smartphones, tablets, and smart TVs throughout the day. Cloud gaming platforms are designed to render the game once on a central server and stream it to any compatible screen, meaning a player can start an intensive adventure game on a desktop at home and instantly continue on a mobile phone during a commute. This fluidity is being facilitated by open standards and strategic collaborations across the industry. This is especially impactful for mobile-centric markets like Asia-Pacific, which holds the largest regional revenue share in the cloud gaming space, where the ease of shifting a game session between a handheld device and a living room TV is a powerful draw for the huge base of smartphone users.

- Application of AI for Enhanced User Experience and Efficiency

The use of Artificial Intelligence and Machine Learning is a rapidly accelerating trend, focused on both enhancing the user-facing gaming experience and optimizing the underlying infrastructure. On the service side, AI is employed to dynamically compress video streams and predict network conditions, which helps reduce latency and maintain stable gameplay even with fluctuating internet quality—a crucial factor for low-latency gaming. Internally, AI is vital for efficient resource allocation in massive data centers, ensuring that the necessary GPU and compute power is instantly available to a user when they launch a high-end title. This backend optimization is a major point of investment for cloud providers. Furthermore, AI tools are beginning to be integrated into game engines for procedural content generation, helping developers to create more dynamic and expansive game worlds with greater efficiency.

Leading Companies Operating in the Global Cloud Gaming Market Industry:

- Utomik B.V.

- Nvidia Corporation

- Numecent Holdings Ltd.

- RemoteMyApp SP ZOO (Vortex)

- Parsec Cloud Inc.

- Paperspace

- LiquidSky Software Inc.

- Simplay Gaming Ltd.

- Ubitus Inc.

- Microsoft Corporation

- Sony

- Amazon web services

- IBM Corporation

- Samsung electronics

- GameFly

- CiiNow Inc.

Cloud Gaming Market Report Segmentation:

By Devices Type:

- Smartphones

- Smart TVs

- Consoles

- Tablets

- PCs

Smartphones hold around 40.2% market share in 2024, allowing users to stream high-quality games without powerful hardware through dedicated applications.

By Genre:

- Adventure/Role Playing Games

- Puzzles

- Social Games

- Strategy

- Simulation

- Others

Adventure/Role-Playing Games (RPGs) immersive games where players assume roles in expansive virtual worlds, engaging in quests and character development, alongside other genres like puzzles and social games.

By Technology:

- Video Streaming

- File Streaming

Video Streaming leads the market with 54.8% share in 2024, enabling high-quality gaming on low-powered devices by processing games on remote servers, while file streaming offers a more bandwidth-efficient alternative.

By Gamers:

- Hardcore Gamers

- Casual Gamers

Casual Gamers lead the market with 52.5% share in 2024, favoring accessible and user-friendly gaming experiences without the need for complex setups, contrasting with hardcore gamers who seek competitive challenges.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia-Pacific accounts for over 47.9% market share in 2024, driven by a growing number of gamers, reliance on smartphones, high-speed internet, and increasing gaming zones in commercial areas.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91-120-433-0800

United States: +1-201-971-6302

Top comments (0)