Dreaming of owning a home in India but earning ₹35,000 per month? Many salaried individuals in this income bracket wonder if a 35000 salary home loan is within reach. The good news is that yes, it is feasible, but approval hinges on several lender-assessed factors. Banks and Housing Finance Companies (HFCs) like SBI and HDFC Bank evaluate your repayment capacity to ensure sustainability.

This article explores what lenders consider, potential loan amounts, required documents, current rates, and tips to enhance your chances. Whether you're a first-time buyer in Mumbai or a family in Bengaluru, understanding these elements can guide your journey towards homeownership.

Understanding Home Loan Eligibility

Eligibility for a home loan isn't just about income; it's a holistic review. Lenders use formulas like the Debt-to-Income (DTI) ratio, ideally below 35% and fixed obligation to income ratio to gauge risk. For a ₹35,000 salary, the focus is on net take-home pay after taxes and deductions, typically around ₹28,000-₹30,000.

Key Factors Lenders Evaluate

Lenders in India, regulated by the Reserve Bank of India (RBI), assess the following:

- Income Stability: Your gross monthly salary of ₹35,000 forms the base, but they verify through salary slips and Form 16. Additional income (e.g., bonuses or spouse's earnings) can increase eligibility by 20-30%.

- Credit Score: A CIBIL score of 750+ signals reliability; scores below 700 may lead to rejection or higher rates.

- Age and Employment: Salaried applicants aged 23-67 with 2-3 years' experience qualify easily; self-employed need 5+ years.

- Existing Debts: Current EMIs (e.g., car loans) should not exceed 50% of income; high obligations reduce loan size.

- Loan Tenure and Amount: Longer tenures (up to 30 years) lower EMIs but raise total interest; LTV ratio caps financing at 90% for loans under ₹30 Lakhs.

- Property Details: The home's value, location, and approval status matter—urban properties often fetch better terms.

- Personal Profile: Education, employer reputation, and residency (Indian or NRI) influence decisions.

How Much Loan Can You Get on a ₹35,000 Salary?

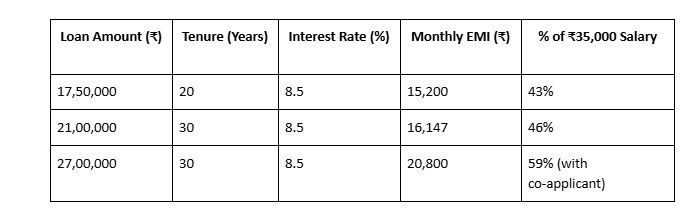

For a 35000 salary home loan, banks multiply monthly income by 50-60 times as a rule of thumb, yielding ₹17.5-21 Lakhs. However, with optimal conditions (high credit score, low debts, 30-year tenure), this can stretch to ₹27-29 Lakhs.

Sample Calculations

Assuming an 8.5% interest rate:

- ₹21 Lakhs over 20 years: Monthly EMI ≈ ₹18,224 (51% of salary—borderline, may need adjustments).

- ₹21 Lakhs over 30 years: EMI ≈ ₹16,147 (46%—more comfortable).

- ₹27 Lakhs over 30 years: EMI ≈ ₹20,800 (exceeds 50%, better with co-applicant). Use an EMI calculator: Input principal, rate, and tenure for precise figures. Down payment (10-20%, or ₹2-5 Lakhs) reduces the borrowed amount, easing approval.

Use an EMI calculator: Input principal, rate, and tenure for precise figures. Down payment (10-20%, or ₹2-5 Lakhs) reduces the borrowed amount, easing approval.

Disclaimer: The sample EMI figures given here are illustrative and based on assumed interest rate, loan amount and tenure only. Actual EMIs depend on the lender’s terms, prevailing interest rates, and individual borrower’s profile. Readers should consult their bank or financial advisor before making any loan decision.

Documents Required for Approval

Preparing documents streamlines the process. Submit these for the home loan:

- Identity and Address Proof: PAN card (mandatory), Aadhaar, passport, or Voter ID.

- Income DProof: Last 3 months' salary slips, Form 16, and 6 months' bank statements.

- Property Documents: Sale agreement, title deed, and NOC from society.

- Others: Passport-sized photos, loan application form, and ITR if applicable.

Digital submission via apps speeds things up; NRIs need additional visa proofs.

Tips to Improve Your Eligibility

To maximise your 35000 salary home loan:

- Enhance Credit Score: Pay bills on time and keep utilisation under 30%.

- Add Co-applicant: Spouse's income can double eligibility and offer tax benefits (₹1.5 Lakhs under 80C).

- Reduce Debts: Clear small loans to lower DTI.

- Save for Down Payment: 20% equity signals commitment.

- Choose Longer Tenure: Lowers EMI but compares total interest.

- Shop Around: Compare via platforms like BankBazaar.

How to Check My Home Loan Eligibility?

Easily check my home loan eligibility online:

- Visit bank sites (e.g., HDFC Bank or ICICI Bank calculators).

- Enter salary (₹35,000), age, expenses, and desired tenure.

- Get instant estimates. E.g., ₹21 Lakhs at 8.5%.

- Pre-apply for soft checks without impacting credit.

Securing a home loan on a ₹35,000 salary is achievable with prudent planning. Lenders focus on your overall financial health, not just income, making preparation key. Start by checking eligibility today, gather documents, and explore rates. Homeownership builds wealth, so take that first step towards stability in India's dynamic property market.

Top comments (0)